Blog

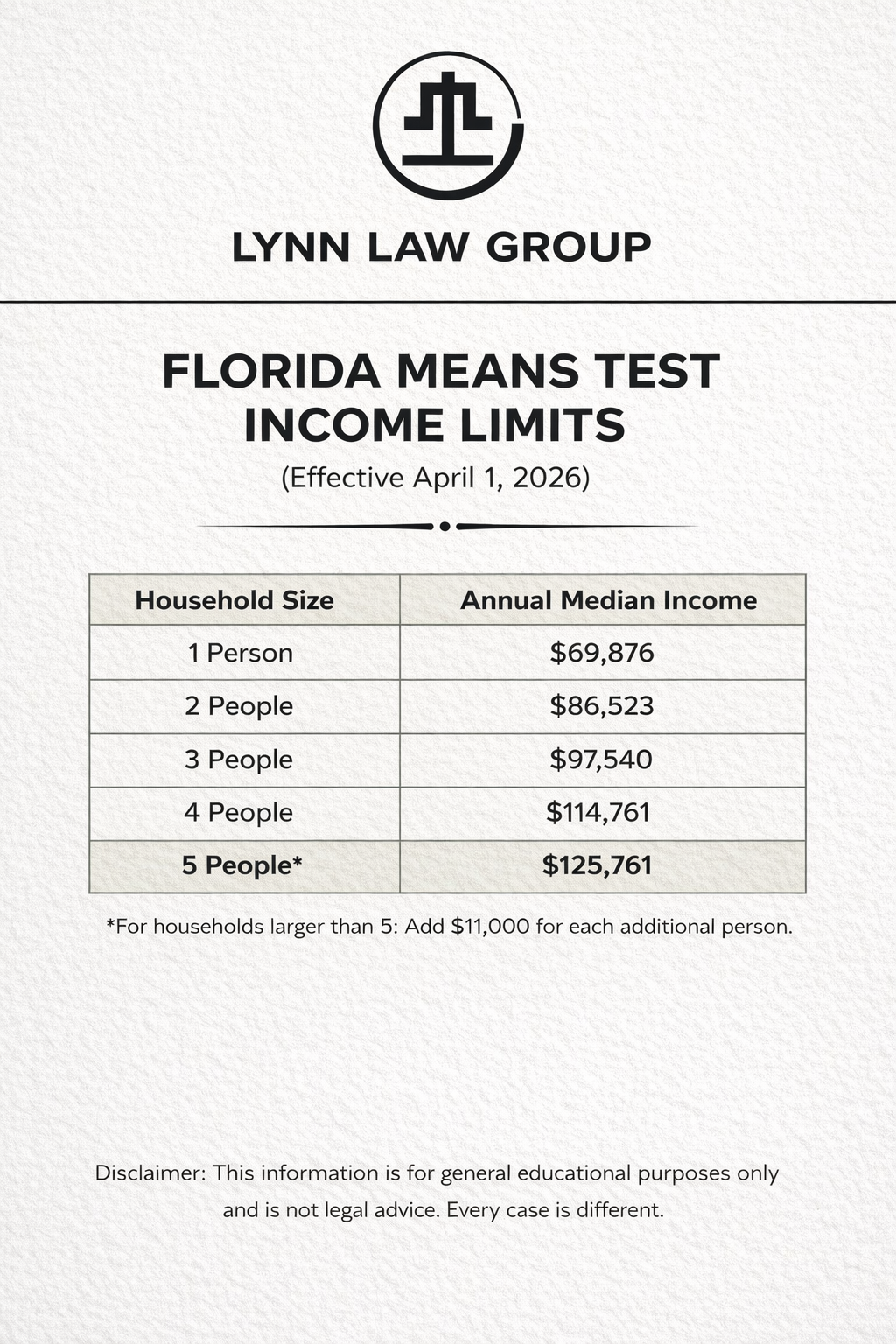

Florida's bankruptcy means test income limits updated April 1, 2026. See the new Chapter 7 income thresholds by household size, learn what changed, and find out if you qualify for debt relief.

Bankruptcy cases don’t pause for spring break. A Fort Myers bankruptcy attorney explains 341 meetings, timing strategy, and what Florida filers need to know right now.

Many people try debt settlement before considering bankruptcy — but it doesn’t always work as expected. Learn the risks, lawsuits that can follow, and when bankruptcy may provide stronger protection for people in Cape Coral and Southwest Florida.

Our bankruptcy attorneys attended the Paskay Seminar to stay current on developments affecting cases in the Middle District of Florida, including Fort Myers, Cape Coral, and Naples.

Valentine’s Day usually focuses on love: relationships, family, connection. But sitting where I sit every day, I see another side of it too. I see people who feel embarrassed to talk about money. People who apologize before they even sit down in my office. People who assume that needing help with debt says something negative about who they are. It doesn’t. Debt is a financial circumstance, a financial condition. It is not a reflection of character, intelligence, or worth. The Quiet Weight People Carry One of the hardest parts of financial stress isn’t always the numbers. It really is the shame that comes with it. I’ve met hardworking professionals, business owners, parents, retirees, and people who did everything “right” but still found themselves overwhelmed. Job loss, medical issues, rising costs, divorce, unexpected emergencies... life has a way of changing the math quickly. Sometimes it is just one life circumstance stacked on top of another one. And yet many people walk in believing they failed personally. They haven’t. Needing a solution doesn’t make someone less responsible. Often, it means they’re finally choosing to face things directly. A Fresh Start Is Not Giving Up There’s a common misconception that bankruptcy is about failure or losing control. In reality, I see the opposite. When someone chooses to learn their options, ask questions, and make a plan, that is an act of strength. It’s choosing clarity over fear. It’s deciding that protecting your family, your peace of mind, or your future matters more than continuing to struggle silently. For many people, the legal protections available through bankruptcy are simply tools... tools that exist so people can reset and move forward. Why This Message Matters The affirmation we shared recently says: Debt does not reduce my worth. I am still lovable, still worthy, and still allowed a fresh start. Choosing clarity is an act of courage. Taking action is an act of self-love. That isn’t just a nice sentiment. It reflects what I see every week in practice. Heck, what I saw today on Valentine's Day in the office. The moment clients understand their options, the shame starts to lift. You can almost see the weight come off their shoulders. Because information creates relief. And relief creates forward movement. If You’re Feeling Stuck If you’re reading this and feeling overwhelmed, here’s what I want you to know: You don’t need to have everything figured out before you ask questions. You don’t have to wait until things become an emergency. And your worth is never measured by your balance sheet. A fresh start isn’t about erasing the past... it’s about building a future that feels manageable again. ❤️ From all of us at Lynn Law Group, we hope this reminder reaches anyone who needs to hear it: financial challenges do not change your value.

Charged Off Debt in Florida: What It Really Means (And Why You Can Still Be Sued) If you’ve checked your credit report and seen the words “charged off,” you might have thought: “Okay, good. It’s gone.” I hear that assumption all the time in my Fort Myers office. But a charge-off does not mean the debt disappeared. It does not mean forgiveness. It does not mean cancellation. And it absolutely does not mean you can’t be sued. Let’s break down what it really means ... especially here in Southwest Florida. What Does “Charged Off” Actually Mean? When a credit card company marks an account as “charged off,” they are making an accounting decision, not a legal one. Typically, this happens after about six months of missed payments. The lender moves the account into a loss category on their internal books for tax and reporting purposes. That’s it. The debt still exists. You still legally owe it. A charge-off simply reflects how the creditor is treating the debt on their balance sheet. Does Charged Off Mean You Don’t Owe the Debt? No. This is one of the most common and most expensive misunderstandings I see. In fact, many collection actions happen after a debt is charged off. Once it’s written off internally, the original creditor may: Send the account to collections Sell it to a debt buyer File a lawsuit Seek a judgment Pursue wage garnishment after Florida judgment (if legally allowed) In Florida, once a creditor obtains a judgment, they can attempt garnishment, bank levies, or other collection remedies depending on your circumstances. So ignoring a charged-off account because you think it’s “gone” can lead to much bigger problems later. Why Lawsuits Often Happen After a Charge-Off Here’s what people don’t realize. After a charge-off, the original credit card company may sell the debt to a third-party debt buyer for pennies on the dollar. That debt buyer’s entire business model is collecting and that is often through lawsuits. We regularly see collection cases filed in: Lee County Collier County Charlotte County Throughout the Middle District of Florida Many people are shocked when they’re served with a lawsuit over an account they believed had already “disappeared.” It didn’t disappear. It changed hands. How Long Can a Creditor Sue You in Florida? Florida has a statute of limitations for credit card debt, but that doesn’t mean a debt becomes unenforceable immediately after charge-off. The clock usually begins running from the date of default, not the charge-off date, and there are nuances depending on the type of contract and the specific facts. This is why timing matters. If you’re unsure whether a debt is still legally collectible, don’t assume. Get clarity. What If the Debt Is Already on Your Credit Report as Charged Off? A charged-off account can remain on your credit report for up to seven years from the date of first delinquency. During that time, it can: Lower your credit score Be sold to multiple debt buyers Trigger collection calls Result in litigation Again, “charged off” is not the same as “resolved.” What Are Your Options in Florida? If you’re dealing with charged-off credit card debt in Fort Myers, Cape Coral, Naples, Lehigh Acres, Bonita Springs, or anywhere in Southwest Florida, your options may include: Negotiating a settlement Defending a collection lawsuit Asserting exemption protections Filing Chapter 7 bankruptcy Filing Chapter 13 bankruptcy Strategic timing to protect assets Every situation is different. Income, assets, home equity, vehicle equity, and prior judgments all matter. This is not something you want to guess about. The Bottom Line: Charged Off Does Not Mean Gone A charge-off is an accounting term. It is not forgiveness. It is not legal cancellation. It is not protection from a lawsuit. If you are overwhelmed by credit card debt, collection notices, or lawsuits in Florida, getting informed early is far less stressful than reacting after a judgment is entered. Work With a Florida Bankruptcy and Debt Attorney I’m Veronica Batt, a bankruptcy and debt attorney based in Fort Myers, Florida. At Lynn Law Group, we help individuals and families throughout: Fort Myers Cape Coral Naples Lehigh Acres Bonita Springs Estero Tampa Orlando Jacksonville throughout the Middle District of Florida All of Florida remotely If you’ve been told your debt is “charged off” and you’re unsure what that means for you, it’s better to ask questions now than deal with a garnishment later. This article is for informational purposes only. It is not legal advice and does not create an attorney-client relationship, you need to discuss your particular situation with a bankruptcy attorney.

Last week, members of the Southwest Florida bankruptcy community gathered to watch the 2026 State of the District Address delivered by the Chief Judge of the United States Bankruptcy Court for the Middle District of Florida. Although the address was presented remotely, our local professionals still came together in person. The Southwest Florida Bankruptcy Professionals Association (SWFBPA) hosted a watch party so attorneys, paralegals, trustees, and financial professionals across our region could hear the updates collectively and discuss what they mean for the people we serve here in Southwest Florida. I’m especially honored this year to be serving as the 2026 Vice President of the Southwest Florida Bankruptcy Professionals Association, an organization dedicated to improving communication, collaboration, and education within the bankruptcy system throughout our local district. A Noticeable Shift: Filings Are Increasing Again One of the realities discussed, and something many of us are seeing firsthand, is that bankruptcy filings have been gradually increasing year over year again That trend isn’t surprising. Families across Florida have been navigating: Higher insurance costs Increased interest rates Rising everyday expenses Fluctuating income in industries tied to housing and tourism In areas like Fort Myers, Cape Coral, Naples, and Bonita Springs, and Estero, these shifts are often felt quickly at the household level. When filings begin to rise, it’s usually not because people suddenly became irresponsible. More often, it’s because the financial margin that once existed has disappeared. For professionals working in this space, that trend is an important reminder: access to accurate information and steady guidance matters more than ever. Why Events Like the State of the District Matter The State of the District Address offers insight into: Current filing trends across the Middle District of Florida Operational updates from the court Emerging issues affecting debtors and creditors Practical realities professionals are seeing across the state Staying informed helps those of us who work directly with individuals and small business owners respond thoughtfully rather than reactively . When the system is functioning well...and when professionals are communicating...it becomes easier for people to stabilize their situation instead of spiraling further into crisis. Offering More Than Legal Answers As filings increase, I’m reminded that the most important thing many people need at the beginning isn’t a legal strategy, it’s simply someone willing to listen, without judgment. By the time most individuals reach out to a bankruptcy professional, they’ve often spent months or even years trying to hold everything together on their own. Many carry a significant amount of stress and, unfortunately, a lot of shame. One of the reasons I’m passionate about this area of law is that bankruptcy exists to provide a lawful, structured path forward. It was designed to give people: Protection Time to regroup Breathing room And ultimately, a genuine fresh start Helping clients understand that this process is a tool (not a personal failure!) is just as important as the legal work itself to me. Especially in times when filings are rising, it becomes even more important for professionals to offer not just technical knowledge, but also patience, clarity, and reassurance, they do call us counselors at law, after all! The Role of the Local Bankruptcy Community One of the most meaningful parts of the SWFBPA watch party was seeing so many different professionals in one room. All people who all play a role in helping the system function fairly. Bankruptcy is never handled by a single person. It requires coordination between: Judges Trustees Attorneys Court staff Financial professionals When those groups stay connected, the process tends to work more smoothly for the individuals at the center of it, the families trying to regain stability. SWFBPA’s mission has always been to strengthen that collaboration here in Southwest Florida, and events like this reinforce why that effort matters. Flipping the Script on the Conversation Around Debt Even as filings rise, many people still hesitate to ask questions because of the stigma surrounding bankruptcy. In reality, most financial hardship is tied to life events or economic shifts, not personal character. Normalizing conversations about debt allows people to: Seek help earlier Avoid unnecessary escalation Preserve more of what they’ve worked hard to build For many Florida families, simply having a safe place to ask questions without judgment is the first step toward real financial recovery. Moving Forward with Purpose Serving as Vice President of SWFBPA this year has reinforced something I see every day: when professionals stay informed, collaborative, and focused on practical solutions, the bankruptcy system works the way it was intended. The goal is never to push someone toward filing. The goal is to make sure that if relief is needed, people understand their rights and their options...and can move forward with clarity and dignity instead of fear. As economic pressure and distress continue to affect households across Fort Myers, Naples, Cape Coral, Bonita Springs, and the surrounding Southwest Florida communities, offering clients a listening ear, steady guidance, and reliable knowledge is more important than ever. For many, that combination is what finally makes a fresh start feel possible. About the Author Veronica Batt is a bankruptcy attorney based in Southwest Florida, serving all of Florida, and currently serves as the 2026 Vice President of the Southwest Florida Bankruptcy Professionals Association. Her work focuses on helping individuals and families understand their financial options, reduce fear and shame around the process, and move toward long-term stability with dignity.

Will People Find Out If I Filed Bankruptcy? One of the most common (and most personal) concerns we hear from clients is this: “If I file bankruptcy, is everyone going to find out?” People worry about their employer. Their family. Their community. They worry about judgment, embarrassment, or the idea that filing bankruptcy somehow becomes public knowledge overnight. Here’s the reality, explained clearly and honestly by experienced Florida bankruptcy attorneys: In the vast majority of cases, no one will know you filed bankruptcy unless you choose to tell them. Bankruptcy Is Not Publicly Announced Yes, bankruptcy is filed in federal court. But that does not mean it is advertised, published, or broadcast in any way. There is: No announcement No public posting No newspaper notice No social media alert No mailing to friends, family, or employers When a bankruptcy case is filed, only two parties are automatically notified: The bankruptcy court Your creditors That’s it. Your employer is not notified (unless you had a prior garnishment, in which case your employer will be very happy to not have to deal with that anymore!). Your family is not notified. Your friends, neighbors, or community are not notified. Unless someone is actively searching federal bankruptcy court records (something most people never do and most attorneys wouldn't even know how to do) they would have no reason or ability to know. Will My Employer Find Out If I File Bankruptcy? This is one of the biggest fears we hear from clients throughout Fort Myers, Naples, Cape Coral, and across Florida. In a Chapter 7 bankruptcy, your employer is not contacted at all. In a Chapter 13 bankruptcy, some cases involve a wage deduction order. If that applies, the notice goes directly to payroll or human resources (not your supervisor) and it does not disclose personal financial details. Just as important: ➡️ Federal law strictly prohibits employers from discriminating against you for filing bankruptcy. Your job is protected. Will Friends, Family, or the Public Find Out? There is no letter sent to your family. There is no notice to your friends. There is no public list circulated. While bankruptcy is technically a public record, it is not something people casually stumble upon. Someone would need to intentionally search federal court databases, know exactly what they are doing, and know who to search for. In real life, that simply doesn’t happen. How Common Is Bankruptcy? Here’s a fact that surprises most people: About 1 in 10 Americans will file bankruptcy at some point in their lifetime. That means: Someone you work with has likely filed Someone in your neighborhood has likely filed Someone you interact with regularly has likely filed You just don’t know - because bankruptcy is far more private and common than people realize. Why Fear and Shame Delay Relief As bankruptcy attorneys serving Fort Myers, Naples, Cape Coral, Miami, and throughout Florida, we don’t see people come in too early. We see people come in years too late...after: Lawsuits have been filed Judgments have been entered Bank accounts have been frozen Wages have been garnished Stress has taken over daily life Not because they didn’t have legal options. But because fear and shame kept them silent. That delay often causes more harm than the debt itself. Bankruptcy Is a Legal Right... It Is Not a Moral Failure Bankruptcy exists for a reason. It is a federal legal tool designed to: Stop collection activity Halt lawsuits and garnishments Protect homes, vehicles, and income Give individuals and families a true financial reset Using the law as it was intended is not something to be embarrassed about. It is informed. It is lawful. And for many people, it is life-changing. The Bottom Line If you’re worried that filing bankruptcy means everyone will find out, take a deep breath. For most people: ✔️ It remains private ✔️ It remains professional ✔️ It stays between you, your attorney, the court, and your creditors If debt stress is affecting your peace of mind, getting accurate information early can make all the difference. This article is for informational purposes only and does not constitute legal advice. Reading this article does not create an attorney-client relationship.

For many people, January doesn’t feel like a “fresh start.” It feels like a financial hangover. The holidays are over. Credit card statements start to arrive. Minimum payments go up because of the holiday spending thrown back on to a credit card. Collection calls resume. Lawsuits and garnishments that paused in December often restart in the new year. And quietly, behind the scenes, something else is happening that most people don’t realize: The timing of a bankruptcy filing...especially early in the year... can significantly affect how much money and protection you keep. This January–March period is one of the most important (and most misunderstood) windows when it comes to bankruptcy planning in Florida. Why Timing Matters More Than Most People Think One of the biggest misconceptions about bankruptcy is that it’s only about how much debt you have. In reality, bankruptcy also looks at timing. When you file, the court examines: Income over specific lookback periods (6 Months) Bank balances Tax refunds Recent payments to creditors Transfers or use of funds That means when you file can be just as important as whether you file. Early planning often creates more options, more protection, and far less stress. The Tax Refund Mistake We See Every Year Between January and March, many people receive (or expect) a tax refund. And the most common instinct is understandable: “I’ll just use my refund to pay down some debt.” Unfortunately, this often backfires and just kicks the can down the road. Here’s why: Partial payments rarely solve the underlying problem Credit card balances often rebound within months The refund is gone, but the debt remains In some cases, using a refund incorrectly can create complications later A tax refund can feel like relief ... but without a strategy, it often becomes a temporary pause, not a solution. How Bankruptcy Treats Tax Refunds (In Simple Terms) In bankruptcy, a tax refund can be considered an asset, depending on timing and circumstances. This does not mean: You automatically lose your refund Filing bankruptcy is a bad idea You should rush or panic What it does mean is that planning matters. Early conversations allow a bankruptcy attorney to: Explain how refunds are treated Look at timing options Avoid last-minute mistakes Protect as much as the law allows Waiting until after a refund is spent...or after accounts are drained out of fear... often removes options that could have existed just weeks earlier. The January–March Bankruptcy Planning Advantage Filing (or even just planning) earlier in the year can offer meaningful benefits, including: More flexibility with timing Better protection of refunds and income Fewer rushed decisions Reduced risk of preference or transfer issues Lower stress and clearer expectations Just as importantly, early planning allows people to move from panic to clarity. You don’t have to decide anything immediately. You just need accurate information. Florida-Specific Considerations Matter Bankruptcy is federal law...but Florida exemptions and local court practices matter a great deal. Issues like: Vehicle equity Homestead protection Household property Income timing are all evaluated with Florida-specific rules in mind. That’s why working with an experienced Florida bankruptcy attorney (especially one familiar with local courts) can make a meaningful difference in outcomes. You Don’t Have to Be “Ready to File” to Benefit From a free Consultation One of the most important things we tell clients is this: A consultation is about information, not commitment or obligation- we aren't used cars salesmen. Many people who reach out in January don’t file immediately. Some don’t file at all. But they leave with: A clear understanding of their options A timeline that makes sense A plan instead of fear That alone can change everything. A Fresh Start Doesn’t Begin With Shame... It Begins With Clarity Debt carries a heavy emotional weight. Shame keeps people silent. Fear causes rushed decisions. But bankruptcy, when used thoughtfully, is a legal financial tool... not a moral failure. If you’re feeling overwhelmed early in the year, this January–March window can be an opportunity to pause, assess, and choose a path forward with dignity. Information brings relief. Planning brings control. And clarity opens the door to a real fresh start. Thinking About Your Options? If you’re navigating debt this January, February, or March, speaking with a knowledgeable Florida bankruptcy attorney can help you understand your rights, your timing, and your options (even if you’re not ready to file).

Enero es el mes en que muchas personas finalmente vuelven a mirar su realidad financiera. Nuevo año. Nuevas metas. Nuevas decisiones. Pero para muchas familias en Florida, el inicio del año también viene acompañado de estrés, deudas acumuladas y una sensación de vergüenza que no deberían cargar. Si estás leyendo esto, déjanos decirte algo desde el principio: no eres solo, la bancarrota no es un fracaso y no es una trampa. Es una herramienta legal creada para ayudar a personas reales, trabajadoras y responsables, a recuperar estabilidad y empezar de nuevo. Esta guía está escrita en español, para nuestra comunidad en Fort Myers, Cape Coral, Lehigh Acres, Naples, Bonita Springs, Miami, Tampa y en toda Florida. El Nuevo Año es un Momento Estratégico para Informarte Muchísimas personas creen que deben “aguantar un poco más” antes de hablar con un abogado de bancarrota. La realidad es que enero es uno de los mejores momentos para informarte. ¿Por qué? El año fiscal acaba de comenzar Muchas demandas y embargos aparecen en los primeros meses del año Hay oportunidades para planificar ingresos y reembolsos de impuestos (los tax refunds) Puedes evitar errores costosos antes de que sea demasiado tarde Hablar con un abogado de bancarrota en español no significa que ya tomaste una decisión. Significa que estás tomando control y que te estas informando. La Vergüenza Mantiene a la Gente Atrapada en Deudas Uno de los mayores obstáculos que vemos no es legal. Es emocional. A muchas personas les dijeron: “Paga aunque te ahogues” “La bancarrota es solo para irresponsables” “Eso arruina tu futuro” Nada de eso es cierto. La mayoría de las personas que consideran la bancarrota: Trabajan Han intentado pagar por años Han usado tarjetas para sobrevivir, no para lujos! Están enfrentando intereses que crecen más rápido que sus pagos La vergüenza no paga deudas. La información sí. ¿Qué es la Bancarrota y Cómo Funciona en Florida? La bancarrota es un proceso federal diseñado para: Detener llamadas de cobradores Parar demandas y embargos Eliminar o reorganizar deudas Dar un camino legal hacia un nuevo comienzo En Florida, los dos tipos más comunes son: 1. Bancarrota Capítulo 7 Elimina la mayoría de las deudas no aseguradas Es más rápida (normalmente 3-4 meses entre someter la bancarrota a la corte y obtener el descargo de deudas, el discharge) Ideal para personas que califican según ingresos y gastos (Means Test) 2. Bancarrota Capítulo 13 Plan de pagos supervisado y estructurado por el tribunal para 3-5 años Protege bienes importantes Útil para personas con ingresos constantes o ciertos activos Puedes modificar tu mortgage (ipoteca para salvar tu casa en muchos casos) Ponerte al día con atrasos en la hipoteca y en los pagos del carro. En ciertos casos, si el vehículo cumple con los requisitos legales y debes más de lo que realmente vale, es posible modificar el préstamo del auto, reduciéndolo a su valor actual y bajando la tasa de interés. También puede proteger a co-deudores que no presentan bancarrota en algunos casos, permitirte ponerte al día con cuotas de la asociación de propietarios (HOA o COA), y ofrecer una descarga más amplia para ciertas obligaciones de divorcio relacionadas con la distribución equitativa. Además, puede ayudarte a ponerte al día con la manutención de menores (child support) y a pagar impuestos atrasados dentro del caso, congelando intereses y penalidades para que los pagos sean más manejables.Cada caso es distinto. Por eso es tan importante hablar con un abogado de bancarrota que hable español y entienda tu situación completa y con mucha experiencia en bancarrota. ¿Qué Deudas Se Pueden Eliminar? Muchas personas se sorprenden al saber que la bancarrota puede eliminar: Deudas de tarjetas de crédito Préstamos personales Cuentas médicas Deudas antiguas Demandas por deudas no aseguradas Y algo muy importante: el proceso detiene legalmente la mayoría de las acciones de cobro y demandas en la corte. ¿Voy a Perder Mi Casa o Mi Carro? Esta es una de las preguntas más comunes. En Florida existen protecciones muy fuertes, especialmente para: La vivienda principal Ciertos bienes personales Ingresos necesarios para vivir En muchos casos, las personas no pierden su casa ni su carro. La exención de vehículo en Florida se aumentó a $5,000 en julio de 2024. Esto significa que hasta $5,000 en equidad en tu carro están protegidos por la ley. Si no tienes una vivienda principal (homestead) que planeas reclamar, esa cantidad puede ser mayor. Esta exención aplica por cada persona que presenta la bancarrota. Pero todo depende de los detalles, y por eso la asesoría correcta es clave. Atendemos a Clientes en Toda Florida (En Español) Aunque nuestra oficina está en el suroeste de Florida, ayudamos a personas en: Fort Myers Cape Coral Lehigh Acres Naples Bonita Springs Estero Miami Tampa Y en todo el estado de Florida Muchos casos se manejan de forma remota, y siempre con atención directa y personal en español. Cuando ustedes nos llaman, no hablan con un call center, van a hablar con un abogado- van a hablar con Veronica o Adrian. El Mejor Primer Paso es Informarte El nuevo año no tiene que ser una repetición del anterior. Si las deudas están afectando: Tu sueño Tu salud Tu familia Tu tranquilidad No tienes que cargar eso en silencio. Hablar con un abogado de bancarrota en español en Florida puede darte claridad, opciones y alivio — incluso antes de tomar cualquier decisión. Un Mensaje Final para el Nuevo Año La bancarrota no define quién eres. Las deudas no definen tu valor. Pedir información no es rendirse — es avanzar. Este año puede ser diferente. Y empieza con conocimiento, no con vergüenza.